BeMined

BeMined

RiskAnalytics

|

Package:

|

RiskAnalytics |

|

Title:

|

Processing of finance data and parallelized quantile lasso regression methods |

|

Version:

|

0.2.0 |

|

Authors:

|

Lukas Borke |

|

Description:

|

Real time processing of Nasdaq and Yahoo finance data and parallelized quantile lasso regression methods |

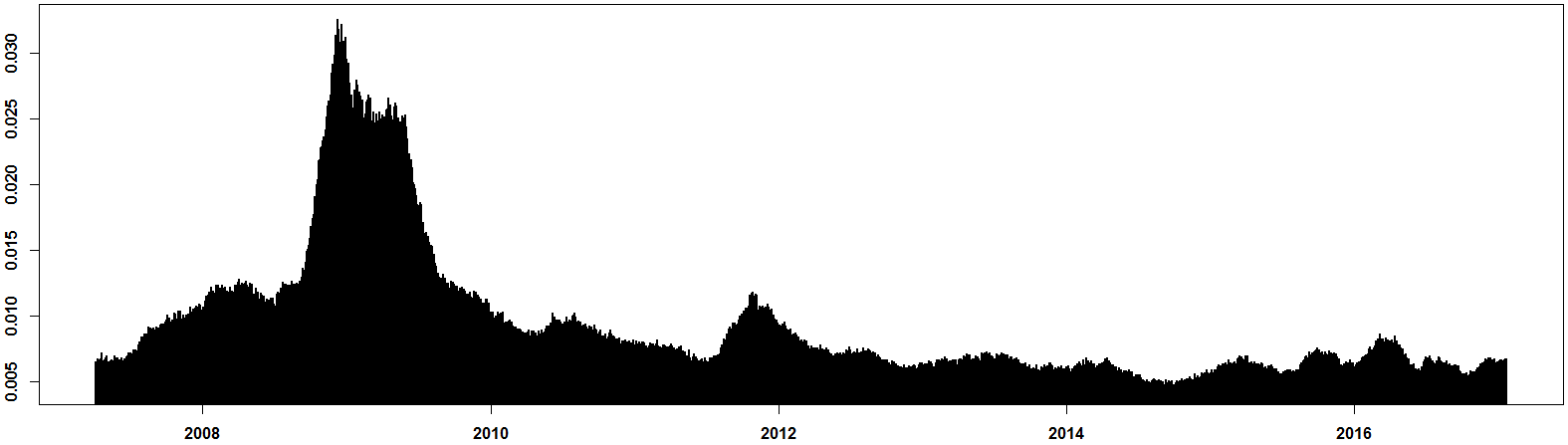

The RiskAnalytics package is a convenient tool with the purpose of integrating lasso penalized quantile regression methods with full solution paths and cluster computing support around the topic "Risk Analytics and FRM". Its main goal is to provide data processing and parallelized quantile lasso regression methods for risk analysis based on NASDAQ data, Yahoo Finance data and some macro variables. The derived "Risk Analytics", which comprise the methods data.analytics, QR.analytics and lambda.analytics, can help to forecast and evaluate the systemic risk for the corresponding markets.

Find out more on the Risk Analytics project in the Risk Analytics section and in the working paper RiskAnalytics: an R package for real time processing of Nasdaq and Yahoo finance data and parallelized quantile lasso regression methods (Borke, 2017).

The plot preview of the FRM lambda time series generated by the RiskAnalytics package.